SVN | Research Economic Update 6.14.2024

1. INTEREST RATES

The Fed’s preferred inflation gauge

- The FOMC voted to leave rates unchanged at its June policy meeting, which aligned with market expectations. On Wednesday, markets braced for the convergence of May’s Consumer Price Index data, which arrived just a few hours before the Federal Reserve’s June policy decision, where policymakers voted to hold interest rates in place.

- Driving the Fed’s decision is a cautiousness about a policy pivot, as while inflation pressures and expectations have come down, they remain above the Fed’s preferred 2% target necessitating a wait and see approach.

- National economic data preceding the Fed meeting showed the US economy and labor market continued expanding. According to the Federal Reserve’s May 29th Beige Book, most Fed Districts report slight or modest growth during the six-week survey period, though two noted no change. Meanwhile, May’s job report from the Bureau of Labor Statistics reported that 272,000 jobs were added in the month, sharply beating expectations.

- According to the Chicago Mercantile Exchange’s Fed Watch tool, two rate cuts remain on the docket this year. However, all will depend on the path of inflation and expectations throughout the second half of the year.

2. SUMMARY OF ECONOMIC PROJECTIONS

- According to the FOMC’s latest summary of economic projections, released at the Fed’s June policy meeting, policymakers see just one rate cut between now and the end of 2024.

- After leaving interest rates steady at 5.25%-5.50% for the seventh consecutive meeting in June, the FOMC’s dot plot showed that policymakers see only one rate cut this year and four in 2025. Projections shifted from the Fed’s last release in March when the dot plot coalesced around a projection of three rate cuts in 2024, followed by another three in 2025.

- Notably, the Fed’s projections differ from those gathered from Fed futures markets, which still forecast two rate hikes in 2024 following the release of the Fed’s latest projections.

- The Fed made no revisions to GDP growth projections and still sees the economy expanding by 2.1% in 2024, 2% in 2025, and 2026. The projection for PCE inflation was revised to 2.6% in 2024, while that for Core PCE inflation was revised to 2.8% in 2024.

3. CONSTRUCTION SPENDING

- US Construction spending fell by 0.1% month-over-month in April 2024, following a 0.2% decrease in March. However, construction spending grew by 10% annually.

- Markets forecasted an increase of 0.2%; however, both private and public spending shrank in April, falling by 0.2% and 0.1, respectively.

- In the public segment, both residential (-0.3%) and non-residential (-0.2%) experienced a decrease during the month. Within the private segment, there was a 0.3% decline in the non-residential, while primarily amusement and recreation fell by -3.5%. The educational segment fell by -3.1% and healthcare by -2.9%. Conversely, the residential segment rose by 0.1%, with spending on single-family projects increasing by 0.1%. Meanwhile, outlays on multifamily housing projects fell by 0.3%.

4. INVESTORS TAKE ON CRE

- A recent Bloomberg review of investor sentiment examines investors’ more candid views on the state of Commercial Real Estate, as the industry remains strong amid a number of emerging risks.

- Standing out is the longer-term risk of higher interest rates. Early on during the Fed’s tightening cycle, there was hope—and market expectation—that interest rates would rise for some initial period of time before coming back down as inflation snapped back toward pre-pandemic levels. However, this hasn’t happened, leaving interest rates higher for longer than some had expected and forcing some shifts in investment strategies.

- CRE assets, which often require refinancing after long loan periods, are susceptible to the recent increases in lending rates, especially those in sectors and places strongly altered by the pandemic, such as downtown office spaces.

- Notably, one take in the article noted that as Fed policymakers keep an eye on CRE risks, they face the reality that the shifts in certain parts of the market largely reflect a secular supply and demand shift caused by the COVID-19 pandemic. As a result, there is so much that monetary policy can sustainably do to address the risks posed.

5. FORECLOSURES RISE

- Data from ATTOM shows a nationwide uptick in foreclosures in May compared to the month before but that foreclosures are down on an annual basis.

- There were roughly 33,000 foreclosure filings in May, up 3.0% from April but down 7.0% from May 2023. The trend signals a mixed market, with pockets of distress emerging in a relatively resilient landscape.

- New Jersey, Illinois, and Delaware posted the highest monthly foreclosure rates. From a metro-level perspective, Chicago, Philadelphia, and Riverside (CA) led foreclosure filings in cities with populations of 1 million or higher. In cities with populations between 200,000 and 1 million, Longview, TX, Trenton, NJ, and Atlantic City, NJ, charted the highest rates of foreclosures.

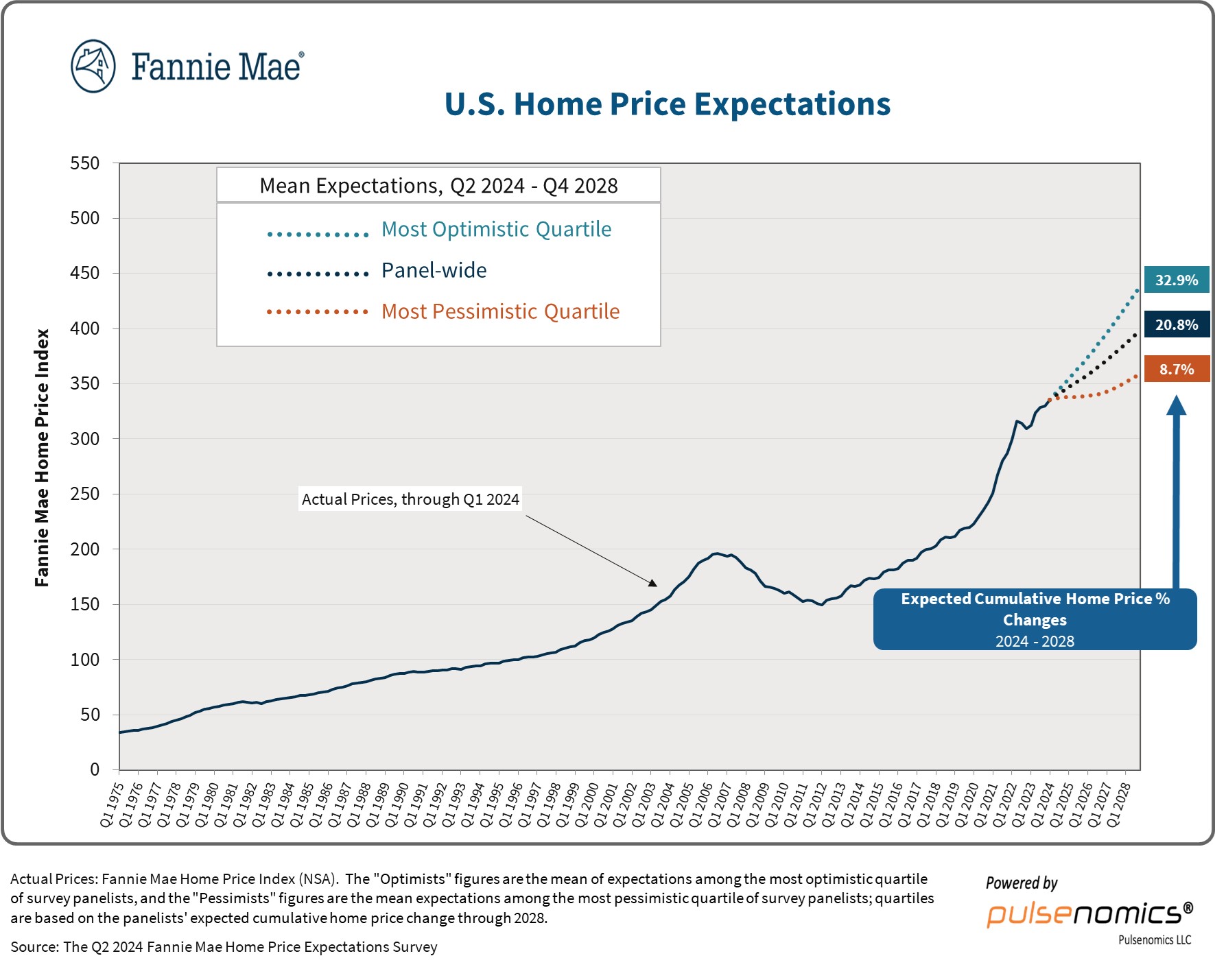

6. HOME PRICE EXPECTATIONS

U.S. Home Price Expectations, Fannie Mae

- According to Fannie Mae’s Q2 2024 Home Price Expectations Survey (HPES), produced in collaboration with Pulsenomics, home price growth is expected to remain robust through 2025.

- The HPES forecasts that US home prices will finish 2024 up 4.3% before slowing to 3.2% in 2025. These projections come off the heels of data from Core-logic in May showing that the nation’s 20 largest metros experienced a record 6.5% annual through March.

- Further, special reporting in Fannie’s analysis details that the “lock-in effect” may be fading. As mortgage rates rose to generational highs, the housing market began to experience a “lock-in effect” where existing homeowners locked into older contracts that were, on average, underwritten with lower interest rates became increasingly incentivized to stay out of the for-sale market.

- Citing data from Realtor.com, newly listed homes are up 12.2% since the start of the year through April. 84% of respondents in the HPES believe that the lock-in effect will continue to diminish and bring more would-be buyers and sellers into the market.

7. CPI INFLATION

- According to the US Bureau of Labor Statistics, the Consumer Price Index for All Urban Consumers (CPI-U) remained steady in May after increasing by 0.3% in April. The consumer price index fell slightly on an annual basis, ticking down to 3.3%, a positive shift relative to earlier in the year but still not enough to sway Fed policymakers further toward rate cuts.

- Core CPI rose by 0.2% in May, its slowest pace since October 2023. Meanwhile, shelter costs rose 0.4% month-over-month, their fourth consecutive month at that level. Gasoline prices fell.

- Overall, markets viewed this month’s report positively, hoping that rate cuts could be on the way with inflation decelerating.

- Still, with policymakers holding rates constant at their June meeting later that day, by the end of the trading day, federal funds futures priced in just two rate cuts between now and the end of the year. The forecast is a significant shift from the three-rate hikes projected as the year began, but markers have gradually recalibrated expectations as inflation pressures persisted.

8. SECOND QUARTER CONSTRUCTION INSIGHTS

- According to data from CoreLogic, Southern states have led the US in building permit approvals for single-unit homes through the second quarter of 2024, with Texas and Florida as key standouts.

- Construction cost growth was similarly higher in the South, coinciding with solid building permit activity. Overall, residential reconstruction costs rose roughly 3% from January to May 2024.

- The price activity for materials In the US has been mixed, with only half of all materials tracked in the report reflecting increases while the rest decreased. Notably, lumber prices have declined by up to 3%, while carpet and clay bricks have risen more than 6.0%.

- Labor costs have also gone up. Through May 2024, roofers, electricians, and painters are each experiencing wage growth above 2% annually. Laborers and insulation installers had the lowest wage growth, but all occupations saw wage growth of at least 1%.

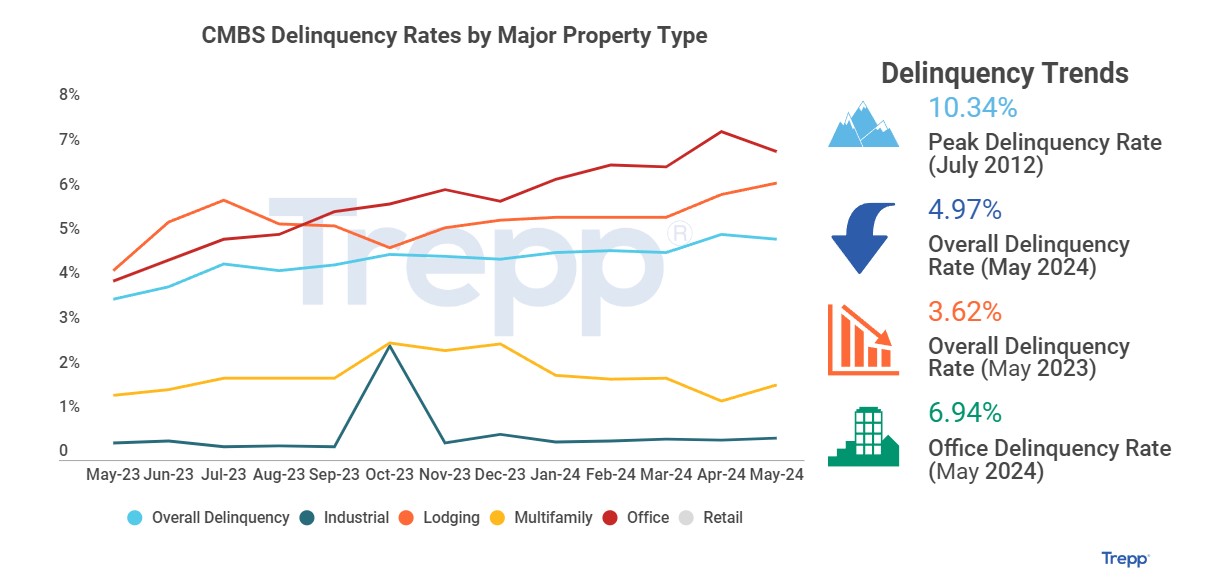

9. CMBS DELINQUENCIES

CMBS Deliquency Rates, Tepp

- According to Trepp, in May 2024, the overall CMBS delinquency rate fell below 5% to 4.97%, driven by significant resolutions in the office sector. Approximately $2 billion in office loans were resolved, reducing the overall delinquency rate.

- However, the impact was offset by $1.2 billion in newly delinquent office loans and new delinquencies in Retail ($995 million), lodging ($238 million), and multifamily ($245 million). Including loans beyond maturity but current on interest, the delinquency rate would be 6.00%. The 30-day delinquency rate rose to 0.35%.

- CMBS delinquency rates remain highest for office properties (6.94%). Lodging (6.22%) and Retail (5.94%) follow closely behind with delinquency rates in the same stratosphere. However, while the retail delinquency rate remains elevated, Retail is the lone sector to have seen improvement in the past year, falling from 6.67% twelve months ago. Multifamily and industrial continue to see the lowest CMBS delinquency rates through May, holding at 1.70% and 0.50%, respectively.

10. MAY JOBS REPORT

- According to the Bureau of Labor Statistics (BLS), the US economy added 272,000 jobs in May, sharply beating the consensus forecast of 185k. However, the unemployment rate rose to 4.0 during the month.

- Employment increases were led by education and healthcare (+86k), government (+43k), and leisure and hospitality (+42k). Construction employment increased by 21,000 during the month.

- Annual wage growth picked up substantially, rising to 4.1% in May, potentially adding to inflation pressures.

- Meanwhile, US job openings dropped to 8.1 million in April, their lowest in over three years, potentially indicating a labor market slowdown. The unemployed-to-job opening ratio decreased to 0.68 — which is still well below 0.93 before the pandemic.

SUMMARY OF SOURCES