1. CPI INFLATION

- The Consumer Price Index (CPI) increased 0.3% month-over-month and 2.7% year-over-year, according to the latest data from the Bureau of Labor Statistics.

- Inflation remained elevated but steady to end 2023, meeting consensus expectations. Meanwhile, core inflation showed signs of moderation.

- Core CPI, which strips out food and energy components, rose 0.2% in December, slightly below expectations of 0.3%. Core CPI rose 2.6% year-over-year, consistent with its November reading and matching its lowest level since 2021.

- Shelter was again the key segment driving inflation, rising 0.4% in December. The Food index rose 0.7% on the month, driven by higher prices for groceries and dining out. Notably, egg prices were down 8.7% on the month.

- The Energy index rose 0.3% month-over-month, while annual price increases slowed significantly compared to recent months.

- Key price declines include used cars and trucks (-1.1%), communication (-1.9%), and household furnishings (-0.5%).

2. DECEMBER JOBS REPORT

- According to the Bureau of Labor Statistics (BLS), total nonfarm payrolls rose by 50,000 during December; a tepid pace of hiring that caps a year of gradual deterioration for the US labor market.

- Both the unemployment rate and the number of unemployed people were little changed in December, at 4.4% and 7.5 million, respectively.

- The most notable gains were in food services and drinking places (+27,000), health care (+21,000), and social assistance (+17,000). The steepest loss of the month was in retail trade positions (-25,000).

- Despite the job market’s relative underperformance, futures markets indicate a low likelihood of a January rate cut. According to the Chicago Mercantile Exchange’s Fed Watch Tool, futures markets grew more hawkish following the employment update.

3. NOVEMBER RETAIL SALES

- According to the latest data from the Census Bureau, US retail sales were stronger than expected in November, rising 0.6% from the previous month to a total of $735.9 billion, following a 0.1% decline in October. Retail sales are up 3.3% year-over-year.

- The increase was driven by a rebound in auto sales alongside robust holiday spending. Sales at sporting goods stores were up 1.9%, followed by miscellaneous retailers at 1.7%, and gas stations at 1.4%.

- Core retail sales, which strip out motor vehicles and parts and include the components used for GDP calculations, rose by 0.5% on the month, beating expectations.

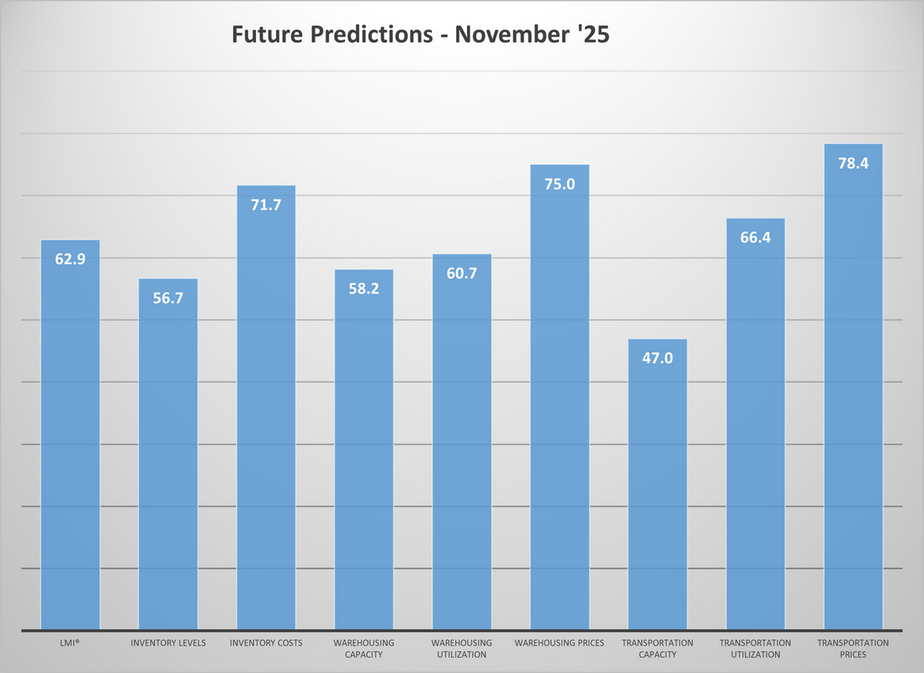

4. LOGISTICS MANAGERS INDEX

- According to the latest data from the Logistics Managers’ Index, US logistics activity fell to 54.2, down 1.4 points from November. An index reading above 50 indicates that the sector is in expansion.

- The sector ended 2025 with its slowest growth in over a year, primarily due to a holiday-driven rundown of inventories. Inventory levels fell to an all-time low of 35.1, dropping by a steep 17.4 points. It was largest month-over-month decline in inventories on record.

- As a result of the inventory depletion, warehouse utilization dropped into contraction territory while warehousing capacity increased.

- Transportation capacity fell sharply to an index reading of 46.9, its lowest level since 2021.

- The tightening of the freight market also led transportation costs to rise for the second consecutive month, climbing to an index reading of 66.7, its highest level in a year.

- Despite the year-end drop off in logistics activity, managers, on average, expect expansion to be stronger over the next few months, with the index of future expectations climbing to 65.3 in December.

5. INSTITUTIONAL INVESTORS IN SINGLE-FAMILY RENTALS

- The White House recently announced that it is considering some restrictions on institutional investments in single-family homes, centered around the argument that such restrictions could reduce competition among individual buyers.

- Generally, economists believe that the impact of such restrictions would be modest and could even reduce the supply of rental homes

- While large institutional investors greatly increased their holdings of single-family homes in the decade-plus since the Great Financial Crisis and housing market crash, they continue to hold a small share of the overall national stock at around 1-to-3 percent.

- Given this small market share, experts suggest that a ban would only have a modest effect on median national prices. However, the impact could be more significant in metro areas where single-family rentals have proliferated more greatly in recent years.

- Most economists believe that the primary driver of high housing costs is a persistent supply shortage. However, to truly tackle this issue, many agree that more construction is needed, and that land use reforms would have a greater impact than institutional bans.

- While the administration has been sparse on details, their argument points out that large investors can move in the market quickly, making it difficult for average homebuyers who rely on financing to compete for available supply.

6. EMERGING INDUSTRIAL MARKETS

- According to recent reporting by Globe Street, several emerging US industrial markets beyond the traditional hubs are attracting increased interest and capital heading into 2026.

- One key standout is Boise, ID. Located along the I-84 corridor with access to the Northern California and the Pacific Northwest, the Boise metro benefits from its proximity to important agricultural and technology pipelines.

- Albuquerque, New Mexico also arises due to its low vacancy and stable absorption rate, despite elevated land and development costs. Built-to-suit projects targeting aerospace, federal government, and advanced manufacturing users have helped underpin local expansion.

- Other emerging industrial markets include El Paso for its rapid inventory growth and role as a logistics ang manufacturing gateway along the southern US border. Omaha, due to its central location and rail connectivity. Then, there’s Dayton, Ohio, which continues to leverage its manufacturing base and strategic location.

7. 2025 REIT PERFORMANCE

- According to reporting by Nareit, REITs ended 2025 on a relatively muted note, with the FTSE Nareit Equity REITs Index falling 2.1% in December and finishing the year with a total return of 2.3%.

- Sector-level performance was mixed in December, led by timberland (+4.5%), lodging/resorts (+0.8%), and gaming (+0.7%). Meanwhile, returns on health care REITs fell in December (-8.4%), as did office (-6.4%), and self-storage (-3.1%).

- At the sub-sector level, apartment returns rose 1.4% in December, followed be regional malls (+1.1%) and shopping centers (+0.7%)

- Health care REITs ended 2025 with the best performance among key sectors, with returns of 28.5%. Industrial and diversified REITs followed, with annual returns of 17.0% and 15.5%, respectively.

- Meanwhile, the FTSE Nareit Mortgage REITs Index (+16.0%) significantly outperformed equity REITs (+2.3%) in 2025, led by the home financing sector (+16.0%).

8. 2026 OFFICE OUTLOOK

- According to a CommercialSearch analysis, the 2026 office industry is beginning to shift from a period of crisis management to a more performance-driven approach in 2026.

- After several years of volality, 2025 brought more clarity on the trend of hybrid work, which has shifted from an experiment to an expectation.

- Hybrid work remained a dominant feature of the sector, but companies have moved from optional office days to a more structured format that includes “anchor days” focused on collaboration and innovation. Offices have been redesigned for flexible zones that can be switched between collaborative and focused work.

- According to the analysis, two converging pressures explain the trend: employees pushing for flexibility and companies seeking to justify real estate costs among a geographically dispersed workforce.

- Meanwhile, capital has begun to reengage with the sector, with a new hierarchy of building performance rather than location coming to define the line between competitive assets and those falling behind.

9. CBO DEMOGRAPHIC PROJECTIONS

- The CBO’s latest demographic projections, released in early January, forecast slower US population growth over the next 30 years compared to previous estimates.

- The new forecast reduces population projections through 2055 by 8 million. The primary drivers of these revisions are lower net migration projections and declining fertility.

- Between 2026 and 2056, the US population is projected to grow from 349 million to 364 million. Growth is expected to slow to 0% by 2056, with population declines expected thereafter.

- The CBO projects that annual deaths will exceed annual births beginning in 2030, with net migration accounting for all population growth from 2030 to 2056.

- The population of those aged 65 and older is projected to grow twice as fast as younger groups, while those 24 and younger is forecasted to decline each year through 2056.

10. JOB OPENINGS AND LABOR TURNOVER

- According to the latest JOLTS report by the Bureau of Labor Statistics, the number of job openings in November was slightly down from the previous month, from 7.4 million to 7.1.

- Over the course of 2025, the total number of job openings fell by 885,000 while the unemployment rate rose from 4.1% to 4.4%

- Hiring activity remained relatively stable in December, with 5.1 million hires recorded. However, the hiring rate dropped to 3.2%, matching its lowest rate in more than a decade outside of the early days of the pandemic.

- Total separations were unchanged at 5.1 million, with 3.2 million quits and 1.7 million layoffs.

- Job openings decreased notably in accommodation and food services (-148,000) and transportation, warehousing, and utilities (-108,000). Openings increased in construction (+90,000).

SUMMARY OF SOURCES

1. FED INTEREST RATE DECISION

- The FOMC cut the benchmark Federal Funds rate by 25 basis points at their December policy meeting. It was the committee’s third consecutive rate cut, widely expected by markets.

- The decision was made along a 9-3 vote, the most divided the FOMC has been on a vote in over six years. The dissenting votes came from both directions: two members preferred no change in rates, while one advocated a larger 50-basis-point cut.

- Fed Chair Jerome Powell again pointed to the cooling labor market as the reason for the cut, but hinted at a potential pause in cuts ahead, claiming that the committee was now “well positioned to wait and see how the economy evolves” before making further moves.

- Separately, the Fed announced it would resume purchasing $40 billion in Treasury bills to ensure there are ample reserves in the financial system. It would be the Fed’s first such purchase since its last round of Quantitative Easing (QE) ended in June 2022.

- However, unlike QE, which aims to stimulate the economy by purchasing short- and long-term bonds and mortgage-backed securities (MBS), the current action is a smaller, more focused effort to stabilize short-term funding markets.

2. FOMC ECONOMIC PROJECTIONS

- In the Summary of Economic Projections that accompanied the December FOMC meeting, officials raised their forecast for 2026 economic growth while lowering their inflation projection. However, it showed a slight uptick in the projected 2026 unemployment rate.

- Compared to their September projections, the FOMC, on average, forecasts GDP growth of 2.3% from 1.8%.

- The committee’s core-PCE inflation forecast for 2026 was lowered to 2.4%, down from 2.6% but still above the 2.0% target level.

- Meanwhile, the new projections showed an average unemployment rate forecast of 4.5% compared to 4.4% in September.

- The employment forecast suggests officials expect levels to remain relatively stable despite expected headwinds; however, more than two-thirds of FOMC members see the risks to unemployment as weighted to the upside.

3. BLACK FRIDAY SPENDING

- US Black Friday retail sales were up 4.1% year-over-year in 2025, according to an analysis by Mastercard Economics. Their analysis measures both in-store and online retail sales across all payment types, but is not adjusted for inflation.

- E-commerce sales grew 10.4% over 2024’s level, while in-store sales grew at a more modest 1.7% pace.

- More consumers are reportedly taking advantage of promotions and shopping earlier in the holiday season compared to last year. Spending on apparel was particularly robust (+5.7%), with in-store sales (+5.4%) up almost just as much as online sales (+6.1%) over the past year. Jewelry sales are up 2.7%.

- Meanwhile, restaurant sales rose 4.5% as dining out has become an increasingly popular part of holiday activities.

4. NATIONAL RENT COLLECTIONS

- On-time rental payments and independently operated rental units ticked up 65 basis points to 83.7% in November, according to the latest Chandan Economics-RentRedi Rent Collections Report.

- While on-time collections remain well below post-pandemic highs, a positive inflection in September suggests a rebound is already underway. The on-time payment rate has now risen for three consecutive months, while the pace of year-over-year declines is moderating.

- Late payments have been the primary driver of underperformance in the mom-and-pop rental sector. The three-month moving average of late payments in independently operated rentals has risen consistently since mid-2024, climbing from a low of 8.4% to a high of 13.2% in August 2025.

- Among the three tracked property types, 2–4-unit rentals led the way in November 2025, posting an on-time payment rate of 84.4%. Single-family rentals (SFR) followed at 83.7%, while multifamily properties trailed with an average on-time collection rate of 82.5%.

- Western states continue to hold the highest on-time payment rates in the country, led by South Dakota, Utah, Alaska, Montana, and Wyoming.

5. LOGISTICS ACTIVITY

- Logistics activity slowed to the most tepid monthly growth rate since June 2024, according to the November update to the Logistics Managers Index (LMI). The LMI is a key leading indicator for Industrial real estate activity.

- The LMI was down 1.7 points from October to 55.7. An index level above 50 indicated expanding logistics activity. While activity remains expansionary, it has slowed significantly in recent months and is most acutely affecting warehousing activity.

- Warehousing utilization contracted for the first time in the index’s nine-year history as the extensive inventories that wholesalers accumulated during the first nine months of the year are gradually drawn down. Consequently, warehousing capacity rose.

- Transportation markets continue to trend upward, with capacity falling and prices increasing.

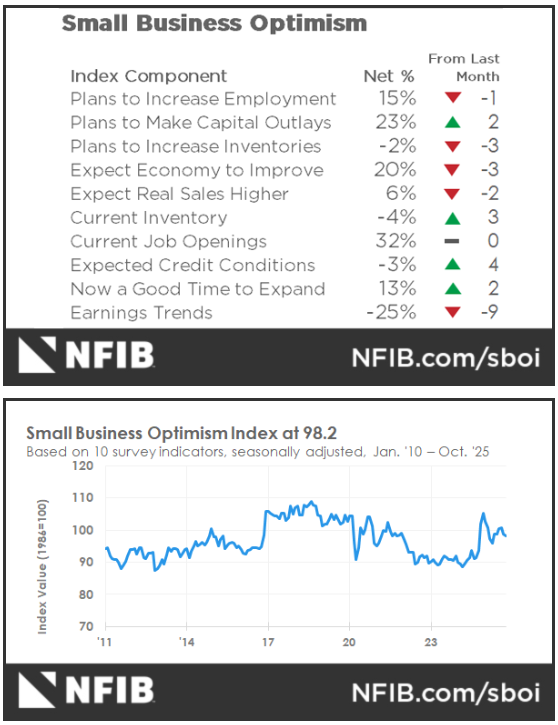

6. SMALL BUSINESS OPTIMISM

- According to the National Federation of Independent Businesses (NFIB), small business optimism rose by 0.8 points in November to an index score of 99. While the score is above the historical 50-year average, optimism remains relatively lukewarm.

- The month-over-month improvement was driven by a rise in the share of owners who expect business conditions to improve over the next six months, up four index points from October.

- However, business owners note several challenges that appear to be tempering their near-term optimism. Inflation remains a core issue, cited by 26% of all respondents, while 38% report having job openings that they cannot fill with qualified labor.

- Expectations for future sales volume fell slightly, as owners were concerned about the sustainability of consumer spending.

7. BEIGE BOOK

- According to the Federal Reserve’s latest Beige Book, published on November 26th, overall economic activity was little changed compared to the previous six-week period across most bank districts.

- Employment growth declined slightly over the period, with about half of the districts reporting weaker labor demand.

- There was an uptick in layoffs, but more firms are using hiring freezes or replacement-only hiring than layoffs. Meanwhile, several employers report adjusting hours worked to accommodate higher or lower expected business volume rather than shift employee headcounts.

- Wages grew at a relatively modest rate, but some sectors, such as manufacturing, construction, and health care, experienced greater wage pressures due to tighter labor supply.

- Price increases were moderate, but cost pressures were widespread in manufacturing and retail. Some Districts noted rising costs for insurance, utilities, technology, and health care.

8. JOB OPENINGS AND LABOR TURNOVER

- Total job openings were roughly unchanged at 7.7 million between September and October, according to recently published data from the Bureau of Labor Statistics. The job openings rate held steady at 4.6%.

- Due to the government shutdown, the September JOLTS estimates are based on partial data self-reported by businesses and released alongside the October data.

- Both hires and total separations were little changed at 5.1 million. Within separations, both quits (2.9 million) and layoffs and discharges (1.9 million) were also little changed.

9. SENIOR HOUSING SELLOFF

- A recent CRE Daily article examines the implications of Blackstone’s exit from the Senior Housing market, following steep losses amid reported operational and market setbacks.

- The exit will force the firm to incur losses of over $600 million from its $1.8 billion senior housing portfolio. The report notes that many properties were sold at over 70% below purchase price as rising costs and pandemic-related challenges impact returns.

- Demographic shifts have made senior housing an attractive niche asset in recent years. Still, its labor and service-intensive nature means that the sector is exposed to specific challenges that may be atypical of other real estate assets.

- As senior housing blends elements of healthcare, hospitality, and housing, it was susceptible to some of the pandemic-driven challenges in those service areas.

- Occupancy rates have tumbled while operating costs are up. Meanwhile, as interest rates rose, loan payments on these properties soared, exposing operators like Blackstone to compressed margins,

- Blackstone’s downsizing began in 2022, and the trend is indicative primarily of post-pandemic challenges that have squeezed returns for existing investors. Looking forward, senior housing fundamentals remain sound thanks to ageing demographics and rising demand.

10. WHERE HOUSING POLICY HEADS NEXT

- As detailed in a recent Chandan Economics deep dive, several legislative developments in Washington may impact housing policy as today’s economic headwinds create space for otherwise difficult political compromises.

- One of the most momentous developments in recent weeks has been a bipartisan push to include housing-related provisions of the bipartisan “ROAD to Housing Act in Congress’s must-pass defense bill.

- Several provisions aim to boost housing supply, including grants for local zoning reform, an expanded federal definition of manufactured housing, and streamlined environmental reviews for small-scale housing developments.

- The House has pushed back on defense bill inclusions, but key members of the House Financial Services Committee are indicating a willingness to advance separate housing-related legislation. Meanwhile, some of the ROAD to Housing provisions appear to have White House backing.

- Meanwhile, the Administration has been evaluating the viability of an IPO for Fannie and Freddie, with a decision potentially coming by late 2025 or early 2026.

- Furthermore, the success or failure of year-end housing policy negotiations will likely sway political positions over HUD funding in January.

SUMMARY OF SOURCES

SHAREABLE FLIPBOOK DOWNLOADABLE PDF

1. EMERGING TRENDS IN REAL ESTATE

- According to the 2026 Emerging Trends in Real Estate Report by ULI-PwC, some of the industry’s key themes heading into next year include the foggy outlook for capital markets, niche asset classes becoming more essential, demographic shifts that will define demand, and the growing influence of artificial intelligence.

- For capital markets, liquidity and sales volume improved in 2025, but expectations for 2026 and beyond vary. Many CRE investors see lower interest rates, abundant debt, and pent-up equity demand as ingredients for short-term capital market expansion, but higher long-term rates and less foreign investment in the longer term.

- Data centers have emerged from a niche asset to an essential property type in 2026, with investors bullish on the growth of cloud computing, enterprise data management, and AI adoption.

- Survey respondents also project that senior housing and other residential subsectors, such as student and manufactured housing, will continue to expand as ageing US demographics create occupancy ripple effects across property types.

- Self‑storage has also evolved as more Americans compromise on size and location when deciding where to live, shifting it into a hybrid lifestyle and investment play.

- The report’s findings also suggest that the office market will remain bifurcated, as trophy buildings in major markets command record rents while lower‑quality properties struggle with high vacancies and depressed valuations.

2. OCTOBER EMPLOYMENT ACTIVITY

- The US private sector added 42,000 jobs in October 2025, while wages rose 4.5% year-over-year, according to the latest ADP National Employment Report.

- In the absence of monthly jobs data from the BLS, the ADP report provides the most current snapshot of national employment trends.

- The October increase marked the first time since July that private employers expanded payrolls. However, hiring remains well below the pace seen earlier this year. Service-providing industries added 33,000 positions, led by trade, transportation, and utilities (+47,000), offsetting losses in professional and business services (-15,000).

- Employers announced 153,074 job cuts in October, up 175% year-over-year and 183% month-over-month. The report notes that industries are recalibrating following the pandemic-era hiring boom, even as AI adoption rises, and consumer spending softens.

3. NATIONAL OFFICE PERFORMANCE

- According to Commercial Café’s National Office Report, the national office vacancy rate was 18.6% in September, 80 basis points (bps) lower than one year before.

- The average listing rate in September was $32.79 per square foot, 0.3% above the September 2024 level. Atlanta ($36.32), Portland ($28.85), and Miami ($56.45) registered the highest listing rates, while Washington, D.C. (+230 bps), Nashville (+220 bps), and the Twin Cities (+190 bps) experienced the largest year-over-year rent increases.

- Manhattan topped the list for year-to-date sales, reaching $5.5 billion through September. The Bay Area followed with $4.3 billion in sales, while Washington D.C. ranked third with $3.2 billion in sales.

- Miami and Manhattan tied for the lowest office vacancy rates in September, each averaging 12.8%.

4. MEDICAL OFFICE BUILDINGS STAND OUT

- An October deep dive by Globe Street suggests that Medical Office Loans continue to stand out for their stability and growth.

- According to Trepp data, CMBS delinquencies in the sector stand at just 6.15% through September, compared to the 11.31% average for conventional office loans.

- The relatively strong performance points to solid fundamentals for the sector. Data from Transwestern shows that medical-office vacancies fell by 20 basis points year-over-year through Q2, compared to a 40-basis-point increase for the traditional office segment.

- Demographic shifts and workforce trends are fueling the relative success of the medical office. According to the Bureau of Labor Statistics, through August, health care-related employment is up from one year prior, while jobs in conventional office-based sectors, such as professional and business services, have declined.

5. CRE TRANSACTIONS STUCK AT PRE-COVID PACE

- According to a recent Moody’s analysis, commercial real estate dealmaking remains relatively sluggish despite a strong start to the fall. Although the dollar volume of CRE transactions is up 5% year-over-year through September, transaction volume remains stuck at pre-COVID levels.

- Transaction data suggest that a flight to quality might be taking shape. The average CRE transaction in September was $12.7 million, up from $11.2 million one year ago.

- Further, zooming in on the 50 largest transactions of the third quarter, all exceeded $73 million, while 29 of those 50 exceeded $100 million, which was a 35% jump compared to the third quarter of 2024.

6. LOGISTICS ACTIVITY

- Logistics sector growth was unchanged in October compared to the month before, according to the latest Logistics Managers’ Index. At 57.4, the current reading indicates a low but steady rate of industry expansion—a reading above 50 indicates that logistics activity is expanding nationwide.

- Expanding transportation activity is driving growth in the sector, offsetting some of the downward pressure from declining inventory and weaker warehousing demand.

- Transportation utilization increased during October, rising 7.3 index points to 57.3. Transportation prices rose 7.5 points to 61.7. Inventory levels contracted slightly on the month (49.5) while warehousing utilization slowed (56.5).

- Taken together, logistics trends suggest that inventories are dropping as holiday sales kick off, easing warehousing demand while increasing transportation utilization.

7. INSURANCE COVERAGE AMONG RENTERS

- A recent analysis by Chandan Economics shows that renters are nearly three times as likely to be uninsured as homeowners (11.7% versus 4.4%) and are more reliant on public plans.

- Just under half of renters (48.8%) have private insurance, while nearly one in three (29%) rely exclusively on public coverage.

- Within the rental market, coverage outcomes vary meaningfully by property type. Single-family renters show the weakest coverage profile—49.2% private and the highest uninsured rate (12.8%). Roughly 16% of single-family renters with private insurance receive a subsidy, compared to an average of 18% among all renters.

- Multifamily renters are the most securely insured, with 51.2% covered by private insurance, while just 9.8% are uninsured.

- With ACA subsidies in legislative play, potential disruption would have a disproportionate impact on renters, particularly those in small buildings and single-family homes, potentially raising delinquency risk and softening leasing velocity.

8. 2026 APARTMENT RENT FORECAST

- According to a recent RealPage analysis, average market-rate effective rents are projected to climb to 2.3% nationally over the next year, a rebound from a 0.7% decline in the year ending in October 2025.

- The analysis points to a broad-based increase in apartment rents, with 11 of the nation’s 50 largest markets expected to see rent gains of 3% or higher.

- Miami (+3.8%), Seattle (+3.7%), Fort Lauderdale (+3.5%), and Los Angeles (+3.2%) topped the list of metros expected to lead the resurgence in growth.

- Several midwestern and coastal cities, including Cincinnati, Columbus, and San Francisco, are also poised for upticks in growth. Each of these three markets is expected to grow by 3.1% annually over the next year.

9. SMALL BUSINESS OPTIMISM

- According to the National Federation for Independent Businesses, small business optimism slipped in October but remains well above its 52-year average.

- Sales and profit expectations fell, with a net 13% of business owners reporting lower sales over the past three months, while a net 25% report negative profit trends.

- Labor shortages remain the top concern affecting small businesses. 32% of owners report having unfilled job openings, while 27% cite labor quality as their most pressing problem —the highest share since 2021.

- Price pressures moderated from the month prior but continue to affect over one in five small businesses. 21% of firms raised their prices in October, with 30% planning to increase them in the coming months.

10. CONSUMER SENTIMENT

- According to the University of Michigan’s preliminary November Consumer Sentiment Index, the index fell 6% from 53.6 in October to 50.3 in the latest reading.

- The decline in sentiment was led by a 17% drop in current personal finances and an 11% decline in year-ahead expectations for business conditions.

- The analysis notes that the federal government shutdown likely contributed to the decline in sentiment, and preliminary findings were made before the shutdown ended.

- Sentiment weakened across most age and income groups, although households with large stock holdings experienced a bump in confidence.

- Short-term inflation expectations edged higher from 4.6% in October to 4.7% while long-run expectations eased from 3.9% last month to 3.6%

SUMMARY OF SOURCES

1. OCTOBER EMPLOYMENT UPDATE

- In lieu of the usual monthly employment report from the Bureau of Labor Statistics, recent private jobs data illustrate persisting labor market weakness during September.

- The ADP National Employment report, which tracks private payrolls, showed a decline of -32,000 jobs during September and follows a reported decline of 3,000 jobs in August. It was the first back-to-back monthly decline in private sector jobs since 2020.

- Elsewhere, online hiring platforms Indeed and LinkedIn reported job posting declines of 9% and 12%, respectively. Meanwhile, government job cuts continue to have an adverse effect on employment growth.

2. FOMC MEETING MINUTES

- Minutes from the September 2025 FOMC meeting reveal that policymakers continued to express a range of concerns despite a mostly unanimous decision to cut the Federal Funds rate by 25 basis points.

- The minutes emphasize recent employment reports indicating that the labor market was softening more than previously thought, particularly due to significant revisions in Spring and early summer employment totals.

- The growing warning signals from monthly employment data convinced most officials on the committee that the balance of risks (labor market vs. inflation) had shifted towards the labor market.

- Nonetheless, inflation worries continue to linger amongst policymakers. A majority of participants still see upside risks to inflation, in part due to recent tariff increases.

- The minutes also highlight divisions among committee members: some voted in favor of the cut but expressed concern that easing could allow inflation expectations to rise. In contrast, others sought a larger, 50-basis-point cut.

3. FED BEIGE BOOK

- US economic growth continued to stall over the past six weeks as labor demand remained muted and input costs rose, according to the Federal Reserve’s October 15th Beige Book update.

- Beige Book responses showed that economic activity nationally has changed little over this period. Three of the twelve Federal Reserve districts reported slight to modest growth, five reported no change, while four experienced a slight decline in activity.

- The latest update reflects a deterioration from the latest Beige Book in August, when one-third of all districts were still reporting modest economic growth.

- Employment conditions remain soft while firms report that prices are rising faster than profits.

- Real estate market conditions were mixed, with the Chicago Fed region reporting an uptick in construction and real estate activity, but most other districts reporting mostly flat activity compared to the previous six-week period.

4. SMALL BUSINESS OPTIMISM

- US small business optimism fell for the first time in three months during September, according to the National Federation of Independent Business.

- Supply chain disruptions and inflation emerged as the key factors reducing optimism among owners during the month.

- 64% of small business owners reported that supply chains were impacting their business to some degree. Meanwhile 14% of small business owners reported that inflation was their single most important problem.

- Earnings stood out as a positive aspect of the report, with respondents reporting their highest earnings since December 2021.

5. CONSUMER SENTIMENT

- According to preliminary estimates from the University of Michigan that were released on October 10th, US consumer sentiment was mostly unchanged from September.

- The index registered a reading of 55.0, a slight dip from September but close to historical lows. A reading above 50 indicates that more consumers view conditions as good than poor.

- The current conditions index modestly improved from September, climbing from an index level of 60.4 in September to 61.0.

- Future expectations fell in October, hovering just above neutral at 51.2. Consumers report declining optimism about the future of their personal finances and buying conditions for durable goods. Inflation expectations fell slightly.

- The report showed little evidence that the ongoing government shutdown is having any material impact on sentiment. However, given that results are preliminary, any potential impact may not be reflected until later in the month.

6. HOMEBUILDER SENTIMENT

- According to the latest NAHB/Wells Fargo Housing Market Index (HMI), builder sentiment was unchanged in September, matching both the August and June 2025 readings for the lowest level since December 2021.

- The September index reading of 32 was below market expectations of 33 and highlights how the housing market continues to perform weaker than expected. A number under 50 indicates that more builders view sales conditions as poor than good.

- Current sales conditions remained steady at a reading of 53, while prospective buyer traffic fell slightly from August to 21. Sales expectations for the next six months rose two points to 45.

- 39% of builders reported cutting prices in September, up from 37% in August, marking the largest share during the post-pandemic period.

7. LOGISTICS ACTIVITY

- Logistics activity fell from August to an index reading of 59.3 in September (a reading above 50 indicated expanding logistics activity), according to the Logistics Managers’ Index (LMI)

- The reading suggests that while logistics activity continues to expand, its growth has slowed significantly. It was the lowest LMI reading in six months.

- Transportation utilization dropped sharply to a neutral reading of 50, a notably weak reading during a typically busy freight season. The index tracking transportation prices slipped below transportation capacity as upstream companies reported weaker price expansion compared to downstream ones.

- Warehousing capacity and utilization each accelerated in September; however, warehousing prices experienced one of the steepest declines of all the individual metrics during the month, falling to a reading of 66.

- Inventory levels expanded (55.2) but at a slower pace compared to August. Inventory costs remained elevated (75.5).

8. FORECLOSURE ACTIVITY

- According to ATTOM’s Q3 2025 Foreclosure Market Report, both foreclosure starts and bank repossessions have seen significant year-over-year upticks. Overall filings were up 17% year-over-year in Q3 to a total of 101,513.

- There were 72,317 foreclosure starts during the third quarter, up 16% from one year ago. The highest number of starts were in Texas, Florida, California, Illinois, and New York.

- 11,723 properties were repossessed during the third quarter, up by a massive 33% year-over-year. Texas, California, Florida, Pennsylvania, and New York registered the highest number of bank repossessions.

- Filings are down 0.3% in September from August, suggesting that foreclosure activity may have peaked despite the annual deterioration.

- The average time to foreclosure is 608 days, down significantly (-25%) from where it was one year ago.

9. SELF-STORAGE RENTS

- After a sustained slump, self-storage rents rose in September, rising 0.3% month-over-month and 0.9% year-over-year, according to data from Yardi Matrix.

- Self-storage REITs are driving the gains. Same-store rents at REIT properties are up 2.6% year-over-year through September, while non-REIT operators saw rents climb just 0.1%

- The average rent stands at 16.80% per square foot, with both climate-controlled and non-climate-controlled units experiencing monthly gains.

- Midwest markets are leading performance on a metro level, led by Detroit (3.6%), Chicago (3.0%), and Minneapolis (2.9%), which are experiencing tight supply and strong multifamily fundamentals.

- Nationwide, 2.6% of the self-storage market is under construction, a slight downtick from August. Sarasota-Cape Coral (FL), Tampa (FL), and Phoenix (AZ) are the most active metros for new supply. Projects under construction represent over 6% of the inventory in these metros.

10. RETAIL TRENDS

- According to the private consumer and market research firm Circana, US retail sales were mostly flat during the five weeks ending on October 5th.

- Circana reports declines across several retail segments from one year ago, including discretionary general merchandise (-3.0%) and non-edible consumer packaged goods (-1.0%).

- All retail dollar-sales gains for the month came from food and beverage, which increased by 1%, but unit sales still fell across all retail segments.

- Circana researchers speak of an “invisible inflation”, where on the surface, retail sales have not realized the impact of inflation, but, in reality, consumers are cutting back on the volume of purchases while still spending the same overall amount.

SUMMARY OF SOURCES

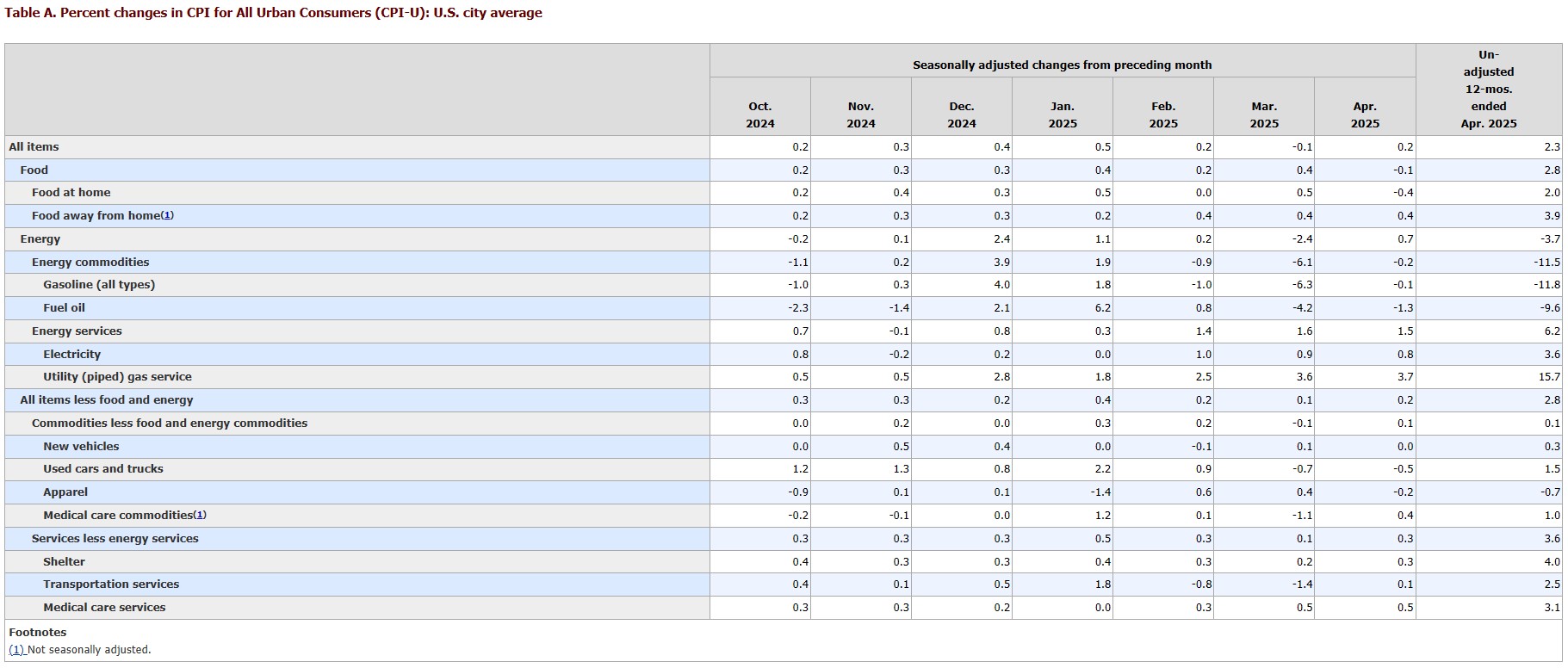

1. CPI INFLATION

- The Consumer Price Index (CPI) rose 0.2% month-over-month and 2.7% year-over-year in July. It marked the third consecutive month that prices accelerated on an annual basis, following three consecutive decreases to begin the year.

- Price pressures rose for items such as used cars and trucks, transportation services, and new vehicles, but fell for gasoline, fuel oil, and shelter. Food prices were relatively unchanged.

- Core-CPI prices, which strip out food and energy and more closely resemble what the Fed considers for monetary policy decisions, were even higher, clocking in at 0.3% month-over-month and 3.1% year-over-year.

- Reemerging core-CPI price pressures, which saw their sharpest rise in six months, add to the notion that tariffs and US trade actions made during the spring are beginning to show their effects on consumer prices.

- Despite the uptick, inflation came in slower than many feared, causing futures markets to raise the probability of a September rate cut from 85.9% one day before CPI was released to 94.2% following the report.

2. FOMC’S JULY INTEREST RATE DECISION

- The FOMC held the federal funds rate unchanged at its July policy meeting, a widely expected decision despite some signs of division about the ideal timing of a potential cut.

- Fed Chair Jerome Powell expressed the majority view on the committee that inflation remained modestly above target, and that while job growth has slowed compared to one year ago, so has labor supply— leaving the labor market relatively balanced, which is reflected in the relatively low headline unemployment numbers.

- Nonetheless, Powell’s remarks came days before a lackluster US jobs report that showed only 75,000 new payrolls were added in July and massive downward revisions for May and June.

- Many officials on the committee continue to note the uncertainty around tariffs and their potentially inflationary effects as a reason to leave rates moderately restrictive. However, while CPI data confirms that these pressures exist, emerging risks to the labor market have significantly increased the likelihood that officials will move forward with a September rate cut.

3. JULY JOBS REPORT

- The US added just 73,000 jobs in July, while May and June saw a combined revision of -258,000, the most significant two-month downward revision since the 2020 onset of the pandemic.

- After the revisions, May’s job growth was revised down to +19,000 from the original +144,000, while June’s payrolls were revised to +14,000 from an initially estimated +147,000.

- Employment trended upward in health care and social assistance, while federal government payrolls continued to decline. The unemployment rate ticked up to 4.2% while labor force participation was unchanged.

- Hiring has dropped across most age groups in recent months, but job postings for entry-level positions are especially weak. July saw the largest increase in the unemployment level among new entrants on record (+275,000) and rose to its highest level since January 2015.

4. THE GEOGRAPHY OF MULTIFAMILY GROWTH

- A recent briefing from Chandan Economics shows that since 2013, apartment household growth in semi-urban communities has outpaced that in both urban and suburban zip codes.

- Between 2013 and 2023, the number of semi-urban multifamily households rose by 25.5% compared to 23.7% in central city districts. Suburban multifamily households grew by a more modest 15.0%.

- While suburban apartment household growth trailed other geographies, it still outpaced total US household growth over the same period, which was just 13.5%.

- Semi-urban multifamily has emerged as one of the sector’s primary growth engines, with room for new construction and a cost structure that remains more favorable than dense downtown areas.

5. GDP

- Real US GDP rose by a seasonally adjusted annualized rate (SAAR) of 3.0% in the second quarter of 2025, following a 0.5% decline during the first quarter.

- Second quarter growth was primarily driven by a decrease in imports and an increase in consumer spending, which was partly offset by declines in exports and investment.

- Though growth came in higher than the first quarter, imports fell by a sharp SAAR of 30.5%, led by a decline in goods imports such as medicinal, dental, and pharmaceutical goods.

- Further, a significant part of the increase in consumer spending was expenditures on non-discretionary services such as health care services. In contrast, an alternative final sales measure that sums consumer spending and gross fixed investment increased by 1.2% compared to 1.9% in the first quarter.

6. LOGISTICS ACTIVITY

- Logistics activity dropped in July, indicating a broader slowdown in the sector as the effects of a new trade normal begin to settle in.

- A deceleration in inventory cost growth primarily drove the decline, as inventory levels expanded at a slower rate than in the spring, leading to a shift in warehousing capacity back into expansion.

- According to the researchers for the Logistics Managers’ Index, each of these shifts was driven by changes in activity by upstream firms or smaller retailers (less than 1,000 employees)

- Downstream and larger firms are reporting falling inventories, increased capacity, and lower price expansion.

- Transportation utilization rose in July while transport capacity and prices remained fairly consistent as freight activity gradually recovers.

7. INDUSTRIAL SUPPLY CLOSE TO PRE-2020 LEVELS

- According to a recent analysis by Commercial Café, the volume of industrial space being built is nearly equal to pre-pandemic levels, though with a different composition.

- 341.8 million square feet of industrial space is currently under construction nationally, while 146.6 million square feet has been completed so far this year.

- E-commerce and omnichannel retail continue to be the primary force driving post-pandemic industrial development, but over-development has pushed up the national vacancy rate.

- The average industrial vacancy rose 50 basis points in July to 9.0%. The vacancy rate is up 290 basis points year-over-year.

- Orange County, CA, charts the highest average in-place rent per square foot, while Dallas-Fort Worth and Houston each doubled their year-over-year pipelines, signaling a new expansion boom in the ‘Texas Triangle’.

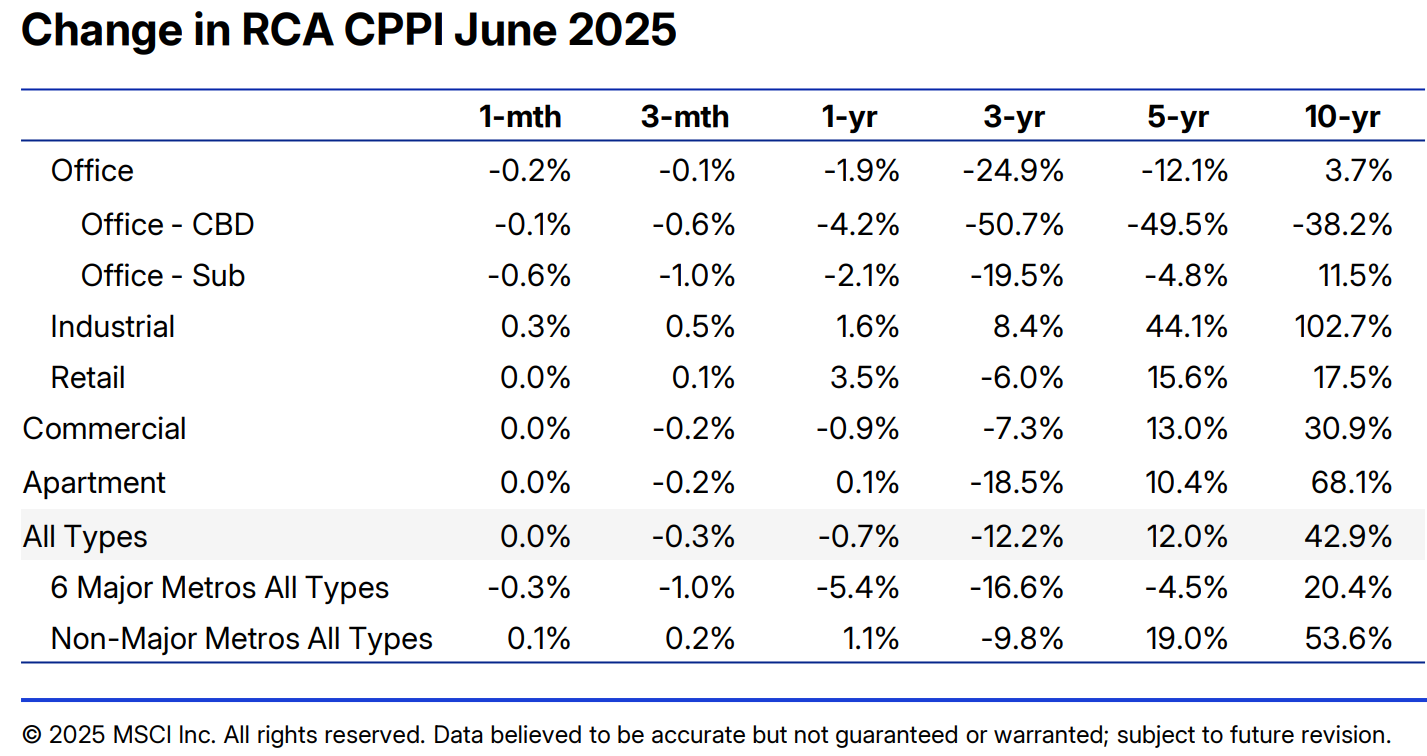

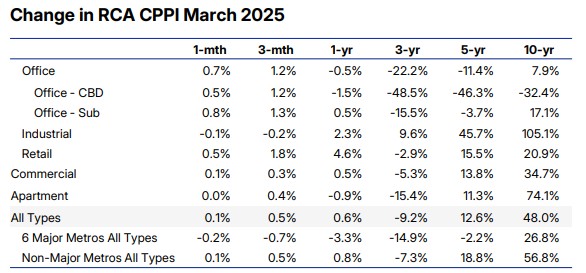

8. COMMERCIAL PROPERTY PRICES

- Commercial property prices were mostly unchanged from June, according to MSCI-RCA’s Commercial Property Price Index; however, prices fell 0.7% year-over-year. The annual rate of decline has slowed substantially over the past two years.

- Retail properties continue to be the leading sector for price growth on an annual basis, climbing 3.5% year-over-year but flat from May.

- Industrial prices climbed 1.6% year-over-year and gained 0.3% from May. Monthly rates in the industrial sector have risen over the past three months.

- Apartment prices posted a 0.1% annual increase in June but were flat on a month-over-month basis.

- Office was the only major property type in June to post a year-over-year decline, falling 1.9% while dropping 0.2% from May.

9. CONSTRUCTION SPENDING

- According to the Census Bureau, US construction spending fell by 0.4% between May and June to a seasonally adjusted annualized rate of $2.13 billion—extending monthly declines that began last November.

- Construction spending has fallen this year as restrictive borrowing rates increasingly limit new real estate demand and curb credit activity for new projects.

- Residential construction plummeted by 0.7% in June to an annualized rate of $952 billion, while non-residential construction ticked lower by 0.1% to an annualized rate of $1.2 trillion.

10. BUILDER SENTIMENT

- Builder confidence in the single-family home market edged higher in July, according to the NAHB/Wells Fargo Housing Market Index.

- Current sales conditions rose marginally, while sales expectations for the next six months saw a higher boost. Reported traffic of prospective buyers fell slightly from June.

- 38% of builders reported cutting prices in July, the highest share since NAHB began tracking the figure on a monthly basis in 2022, following a previous record high in June. The share of builders cutting sales prices has gradually climbed over the past several months

- The average sales price reduction was 5% in July, on par with cuts seen since last November

SUMMARY OF SOURCES

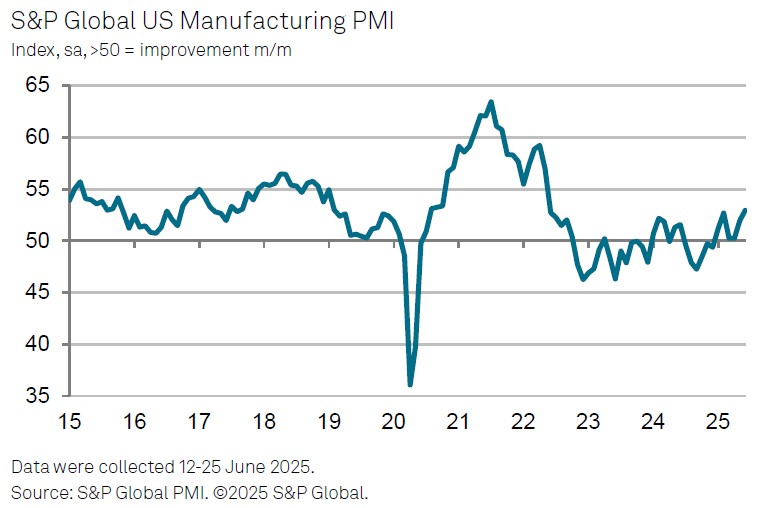

1. FACTORY ACTIVITY EXPANSION

- US factory activity experienced its sharpest expansion in over three years during June, according to indicators from S&P Global and the US Census Bureau.

- According to the Census Bureau, new orders for manufactured goods increased by 8.2% in May and have risen in five of the past six months.

- More recently, the S&P Global US Manufacturing PMI indicates a significant expansion in US factory output during June, driven by a combination of increased new orders and a surge in exports.

- The Manufacturing PMI also indicates that higher demand for capacity prompted firms to increase staff the most since September 2022. Meanwhile, input costs accelerated the most on a monthly basis in nearly three years.

2. ONE BIG BEAUTIFUL BILL ACT AND CRE

- On July 4th, President Trump signed into law the ‘One Big Beautiful Bill Act’, a sprawling tax and spending bill with several provisions related to Commercial Real Estate but with complex, not easily defined implications.

- Key among them is the permanent establishment of Opportunity Zones, which will now operate in 10-year cycles with stricter eligibility requirements than previously.

- A return of 100% bonus depreciation has been celebrated by many in the real estate industry, expected to drive significant tax savings by enabling owners to deploy it strategically for certain building purchases and tenant improvements.

- The law also alters the calculation of Adjusted Taxable Income, allowing for the addition back of depreciation, amortization, and depletion, which is expected to increase the basis for deducting interest expenses.

- Others view the law as mostly neutral for Commercial Real Estate, with some increases in SALT deductions potentially becoming a boost to real estate values, while deep spending cuts could partly offset this with weakened demand.

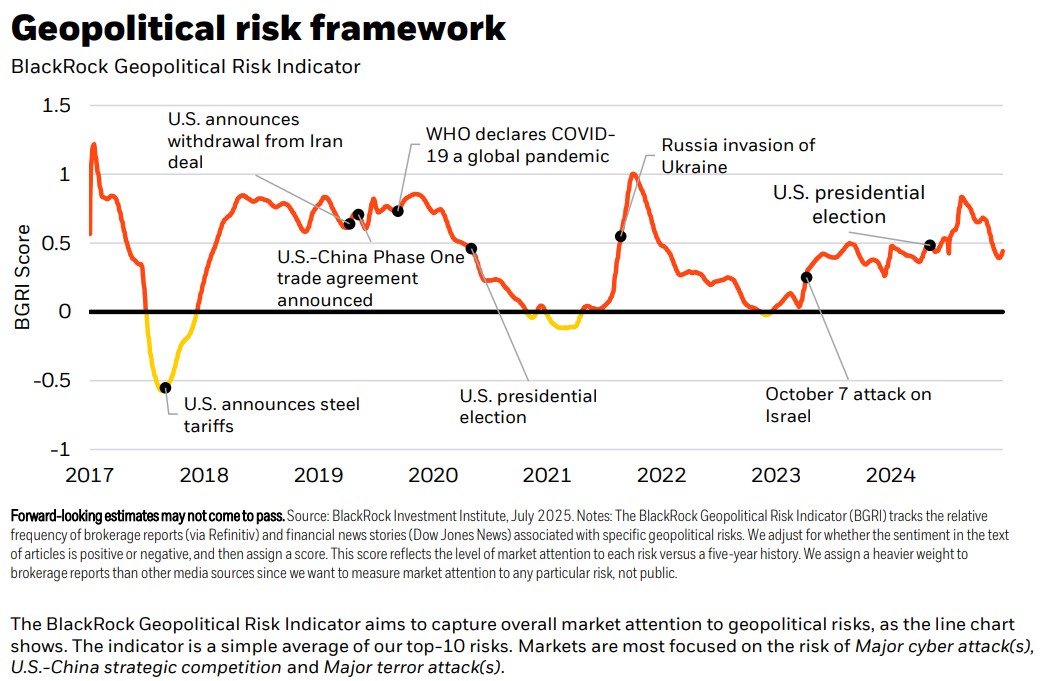

3. GEOPOLITICAL RISKS

- According to BlackRock’s tracking of market attention to geopolitical risks, the risk of global trade protectionism remains the issue that drives the most attention from financial markets, out of those tracked. At the same time, concerns around the Middle East have increased in recent months.

- Uncertainty and volatility have dominated the geopolitical landscape in 2025, but have impacted markets to varying extents. Global trade risks remain the scenario most likely to materialize, as despite a pause to several tariffs and ongoing trade negotiations, the market expects effective tariff rates to stay above 2024 baselines.

- The outbreak of war between Israel and Iran in June, which saw direct US involvement, threatens both regional and global energy market stability. While a recent ceasefire has dampened market attention to these developments, BlackRock still views these risks as high, given the uncertainty surrounding damage to Iran’s nuclear program and the mutually incompatible red lines between the parties involved.

- The US-China strategic competition risk remains high despite some signs of progress on trade talks between the two nations in June. Both countries continue to take steps toward export controls and decoupling of key technology sectors, while hawkish sentiments in each government raise the chances of military miscalculation.

4. LOGISTICS ACTIVITY

- US logistics activity rose only modestly in June but reached its third-highest reading in the past two years, according to the latest reading of the Logistics Managers’ Index (LMI).

- Supply chain activity during the first half of 2025 has somewhat defied typical seasonal patterns. The only months when logistics activity expansion has been higher over the past two years were January and February of this year, which resulted from wholesalers rushing in new orders to get ahead of potential tariffs.

- While activity later reverted to its pre-January trend, it continued to expand healthily, growing in each month since March.

- June’s increase in the LMI was primarily driven by a sharp rise in inventory levels during the first half of the month as importers took advantage of a pause in many punitive tariffs.

- Inventory costs rose significantly as a result, reaching their highest level since October 2022, when supply chains were still dealing with COVID-related disruptions.

5. MORTGAGE APPLICATIONS RISE

- Mortgage applications soared by 9.4% during the week ending on July 4th, 2025, according to data from the Mortgage Bankers’ Association.

- Application volumes have now grown for three consecutive weeks, marking their longest streak of expansion since December 2024, at a time when benchmark mortgage rates were softening.

- Both refinance applications, which tend to be more sensitive to short-term interest rate changes, and purchase applications jumped by 9% during the week.

- Refinance applications are up 56% from the same time last year, while purchase activity is up 25%—a key signal that housing market activity is gradually thawing.

6. JUNE JOBS REPORT

- The US economy added 147,000 new jobs in June, narrowly above May’s revised total of 144,000 additions, according to the latest data from the Bureau of Labor Statistics (BLS). The unemployment rate ticked down to 4.1%.

- Job growth has been steady during the first half of 2025, proving resilient in the face of rising economic uncertainty over the past several months, including the rise of AI investment and increasing trade and geopolitical tensions.

- Following the release of the June jobs report, the probability of a July rate cut by the Federal Reserve reduced considerably. June’s job data appeared to validate policymakers’ wait-and-see approach further, causing futures markets to revert toward a projection of fewer and further-out rate cuts.

- However, the June jobs report showed government jobs accounted for a significant share of June’s growth, with strong state and local hiring leading to a 73,000 increase in public sector roles.

- The private sector still added 74,000 jobs in June, according to initial estimates. Still, these more subtle shifts in the labor market will be key to policymakers’ assessment of how rate policy should evolve.

7. COMMERCIAL PROPERTY PRICES

- Commercial property prices fell 0.2% month-over-month and 1.0% year-over-year in May, according to the latest Commercial Property Price Index (CPPI) update from MSCI-RCA.

- Nationally, commercial property prices extended a trend of mild annual decreases experienced over the past year, with the index posting its fifth consecutive monthly decline.

- Retail led all property types during May, rising 0.2% from April and 4.0% year-over-year. Retail prices have risen monthly for 12 consecutive months.

- Industrial prices declined by 0.2% and rose just 0.1% year-over-year as the sector’s post-pandemic momentum continues to fade. May marked the seventh consecutive monthly decline in industrial prices.

- Apartment prices fell 0.4% from April and experienced a 1.1% drop year-over-year. Declines in Apartment prices have moderated somewhat in the past year and are gradually trending more positively.

- The CBD Office sector continues to be the weakest tracked property sector, but the pace of decline eased in May. CBD office fell 0.4% from April and is down 6.2% year-over-year, a significant improvement over a nearly 30% decline this time last year.

- Suburban Office prices climbed 0.4% month-over-month and are up 1.5% year-over-year.

8. BUSINESS OPTIMISM

- Business optimism was mostly unchanged in June from a month prior but fell slightly below forecasts, according to the latest data from the National Association of Independent Business (NFIB)

- There was a substantial increase in respondents reporting excess inventories, which drove a slight decline in the overall index month-over-month. Meanwhile, the net percent of business owners expecting better business conditions also fell, dropping three points to 22%.

- The net percentage of owners expecting higher sales volumes ahead fell three points to 7%, while a net 21% of owners plan capital outlays in the next six months, down one point from May.

- Business uncertainty also declined in June, while the share of small business owners reporting taxes as their single most important problem rose 19%, its highest since July 2021.

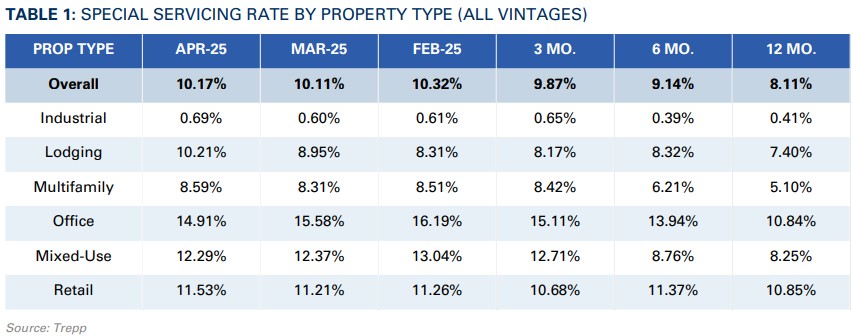

9. CMBS DELINQUENCIES RISE

- According to Trepp, the CMBS delinquency rate rose five basis points to 7.13% in June, with four of the five main property types registering increases during the month.

- The highest delinquency rate increase during June was in the Office sector, which climbed 49 basis points to 11.09%, reaching a record high and surpassing previous peaks in July 2012 and December 2024.

- Lodging continued to display volatile delinquency trends, rising 42 basis points to 6.81% after shedding nearly 150 basis points during May, according to the report.

- The delinquency rate for Industrial loans ticked up just three basis points and remains at an industry low of 0.51%. The Retail delinquency rate climbed by five basis points to 6.69%.

- Multifamily loans were the only major property sector to buck the trend, with the delinquency rate falling by 20 basis points from May.

10. APARTMENT SUPPLY TRENDS

- A new analysis by RealPage suggests that many large construction markets have reached their peak, but that at least 13 of the nation’s 50 largest apartment markets won’t reach their highest supply volumes until at least the second half of 2024.

- The report identifies Boston, Detroit, Fort Lauderdale, Kansas City, and Memphis as metros expected to hit their construction peaks during the third quarter of this year. Cleveland, Columbus, and New York are expected to peak during the fourth quarter.

- Looking ahead to 2026, Newark is expected to reach its high during Q1, while Anaheim, Los Angeles, and San Diego are projected to reach their supply peaks in Q2. Finally, Greensboro, NC, is expected to peak during Q3 2026.

SUMMARY OF SOURCES

1. FED INTEREST RATE DECISION

- The Federal Reserve’s FOMC held rates unchanged at 4.25%-4.50% during its May policy meeting, aligning with market expectations leading up to the decision.

- While markets and experts largely expected the FOMC to keep rates steady in May, some expressed concern about leading anecdotal data, such as the Beige book, recently pointing to deteriorating conditions in the labor market, arguing that there could be room for a pre-emptive rate cut.

- However, despite Fed Chair Jerome Powell referencing the “great deal of uncertainty” around tariffs during his post-meeting press conference, he said that policymakers need not “be in a hurry to adjust its monetary policy” and that to wait-and-see remains “the appropriate thing to do.”

- Notably, within a few days of the May FOMC meeting, the Trump administration announced a 90-day pause on its ‘reciprocal tariffs’ against China. As a result, the CME fed futures markets are, on average, forecasting delayed and fewer rate cuts in 2025 relative to before the announcement of a tariff pause.

2. CPI INFLATION

- CPI inflation eased on an annual basis to 2.3% in April, its lowest annual reading since February 2021. Prices climbed 0.2% on the month.

- Core CPI prices increased 0.2% month-over-month and 2.8% year-over-year.

- While monthly readings edged higher compared to March, they largely fell short of market expectations and were seen as a positive sign in the face of fear of potential tariff-induced inflation.

- Shelter costs rose 0.3% during the month, accounting for more than half of the monthly gain in headline CPI.

- Energy prices rose by 0.7% month-over-month, driven by a rise in natural gas and electricity costs, while gasoline prices declined. Meanwhile, food prices fell by 0.1% in March.

3. SMALL BUSINESS OPTIMISM

- Small business optimism declined in April, according to seasonally adjusted data from the National Federation for Independent Businesses (NFIB).

- Optimism remained below its historical average for a second consecutive month as fewer owners expect to increase business investments in the near term.

- The net share of small business owners who expect better business conditions fell six points to a net 15% in April, its lowest share since October 2024.

- 34% of business owners expressed doubt in their ability to fill existing job openings, down percentage points from March. Interestingly, job openings are at their lowest level since January 2021.

- A net -4% of owners plan inventory investment in the coming months, down three points from March and its lowest reading since June of last year.

- 18% of owners are planning capital outlays in the next six months, down three points from March and its lowest since the depth of the COVID-19 pandemic in 2020.

- The most recent survey, conducted in April, does not capture the effect of the Administration’s announcement of a pause in its China tariff policy, which could meaningfully boost sentiment in the coming weeks.

4. CONSUMER CONFIDENCE

- According to data from the Conference Board, consumer confidence fell by 7.9 points in April to an index level of 86.0, its fifth consecutive monthly decline.

- Both consumers’ assessment of current business conditions and their short-term outlook for conditions shifted toward the downside, with the expectations index reaching a 13-year low.

- Forward-looking expectations deteriorated across the board, including expectations regarding future business conditions, employment prospects, and future income.

- Further, the share of consumers who expect fewer jobs in the next six months sits at 32.1%, roughly as high as in the middle of the Great Recession.

- The fall in consumer confidence was also broad demographically, falling amongst all age and most income groups and shared across all political affiliations.

- The decline was sharpest among consumers 35-55 years old and those making more than $125,00 per year.

5. CONSTRUCTION SPENDING

- US construction spending shrank by a seasonally adjusted 0.5% month-over-month in March, according to the latest available data from the US Census Bureau.

- High mortgage rates and tariffs on imports contributed to both a supply and demand-driven increase in construction costs, constraining homebuilding activity during the month.

- Private sector spending fell 0.6% in March, driven by pull-backs in both non-residential investment (-0.8%) and residential investment (-0.4%).

- Public sector spending fell 0.2%, primarily due to a fall in non-residential investment and reduced spending on power, commercial, and amusement and recreation construction. Office and transportation construction experienced some of March’s most significant spending increases.

- Annually, US construction spending is up 2.8% through March.

6. SPECIAL SERVICING RISES IN APRIL

- According to Trepp, the special servicing rate for CMBS loans rose six basis points (bps) to 10.17% in April.

- While April’s increase was relatively modest, the industry-wide special servicing rate sits well above the 8.11% charted one year ago and the 5.62% registered in April 2023.

- There were significant variations in sector-level performance during the month. Lodging continued to chart the most significant increase, climbing 126 bps to 10.21% in April and following a 64 basis point jump in March.

- Multifamily and Retail also saw special servicing rates climb during the month, rising roughly 30 basis points each. Industrial rose just nine bps.

- Office saw some relief as its rate dropped by 68 basis points, a repeat of March, to 14.91%.

7. LOGISTICS MANAGERS’ INDEX

- Logistics activity rose in April following a slowdown in March, according to the latest reading of the Logistics Managers’ Index.

- Logistics activity was elevated to start the year as North American firms attempted to front-run a potential trade war before snapping back in March. April’s rebound reflects a growth level more consistent with logistics sector performance before the 2024 Presidential Election.

- Inventory levels rose but at a much slower pace compared to activity experienced during the first quarter, reflecting a more normal seasonal inventory buildup.

- Despite lower inventory growth, warehousing prices and inventory costs climbed faster than the previous month, suggesting that much of the first-quarter inventory buildup remains sitting in storage facilities.

8. COMMERCIAL PROPERTY PRICES

- Commercial property prices rose 0.6% year-over-year in March as commercial real estate gradually edges into a faster pace of annualized growth. Further, a quarter-over-quarter gain of 0.5% during Q1 puts the pace of annualized growth at 1.8%.

- According to the monthly update by MSCI-Real Capital Analytics, CRE prices have not yet responded to the spike in uncertainty that has accompanied recent trade negotiations and policy rollouts.

- Rather, CRE still exhibits the uneven price performance across sectors that has persistent since 2022.

- Retail led all sectors during Q1, rising 1.8% from Q4 2025 and 4.6% year-over-year.

- Industrial, which has typically seen the strongest price growth of any sector during the post-pandemic period, followed Retail with a 2.3% year-over-year increase during Q1 but declined 0.2% from Q4.

- Apartment prices declined 0.9% year-over-year during Q1 but climbed 0.4% quarter-over-quarter, its second consecutive quarter of growth, suggesting that price stagnation is gradually thawing in the sector.

- CBD office prices were down just 1.5% year-over-year in Q1, a significant turnaround from the more than 30% recorded one year ago. Suburban office prices rose 0.5% year-over-year during Q1.

9. GDP

- Real US GDP contracted at an annualized rate of 0.3% during the first quarter of 2025, based on the advance estimate from the US Bureau of Economic Analysis.

- The first-quarter decline was primarily due to a sharp increase in imports, which is a negative factor in the GDP calculation. GDP’s other components—consumer spending, investment, and exports—each also increased, partly offsetting the downside effect of imports.

- Beneath the surface, the US economy still exhibits strong fundamentals. The rise in imports during the first quarter was significantly driven by US firms and consumers, who front-loaded their purchases of goods in anticipation of the Trump Administration’s tariffs.

- It reflects robust consumer spending despite softening consumer sentiment. Nonetheless, the first-quarter numbers indicate that consumers and producers significantly adjusted their activities in anticipation of heightened trade tensions.

10. APRIL JOBS REPORT

- The US Economy added 177k payrolls in April, above consensus estimates of 130k, according to the Bureau of Labor Statistics (BLS). The unemployment rate was unchanged at 4.2%.

- It was a strong showing for firms despite being a month headlined by heightened economic uncertainty and volatility. April’s job growth slightly edged out the average monthly increase of 152k over the previous 12 months.

- Payrolls grew the most in the healthcare sector (+51k), transportation and warehousing (+29k), and financial activities (+14k). The increase in transportation and warehousing employment comes after little change in March and arrives after an uptick in logistics activity, including imports and inventories, to start the year. Federal government employment continued to decline (-9k).

SUMMARY OF SOURCES

SHAREABLE FLIPBOOK DOWNLOADABLE PDF