According to the US Bureau of Labor Statistics (BLS), the Consumer Price Index (CPI) increased 0.2% month-over-month (MoM) in August, repeating July’s pace and in line with the consensus forecasts that led up to the data release.

The annual CPI measure fell for the fifth consecutive month to 2.5%, its lowest since February 2021.

Over the past 12 months, energy prices have been the main force driving down the headline inflation rate, which is down by 4% year-over-year (YoY). Transportation prices have also kept the inflation rate elevated, up 7.9% annually, yet they have decelerated from the previous month.

Core-CPI inflation, which excludes the more volatile food and energy components from the index, rose by 0.3% MoM in August, marginally above July’s 0.2% pace.

Monthly, core inflation was higher than expected, boosted by an acceleration in shelter and airfare price increases. Annually, core price inflation matched its three-year low of 3.2% reached in July.

Shelter remains the critical component of CPI, which is still elevated on an annual basis and continues to accelerate — up 5.2% YoY and up ten basis points from July. Airfare price acceleration can be attributed to more robust travel demand during the summer, which should ease in the coming months.

While the PCE price index is the Federal Reserve’s preferred measure of inflation for influencing monetary policy decisions, August’s CPI report is more evidence that inflation is trending downward and likely cements the outlook for a September rate cut.

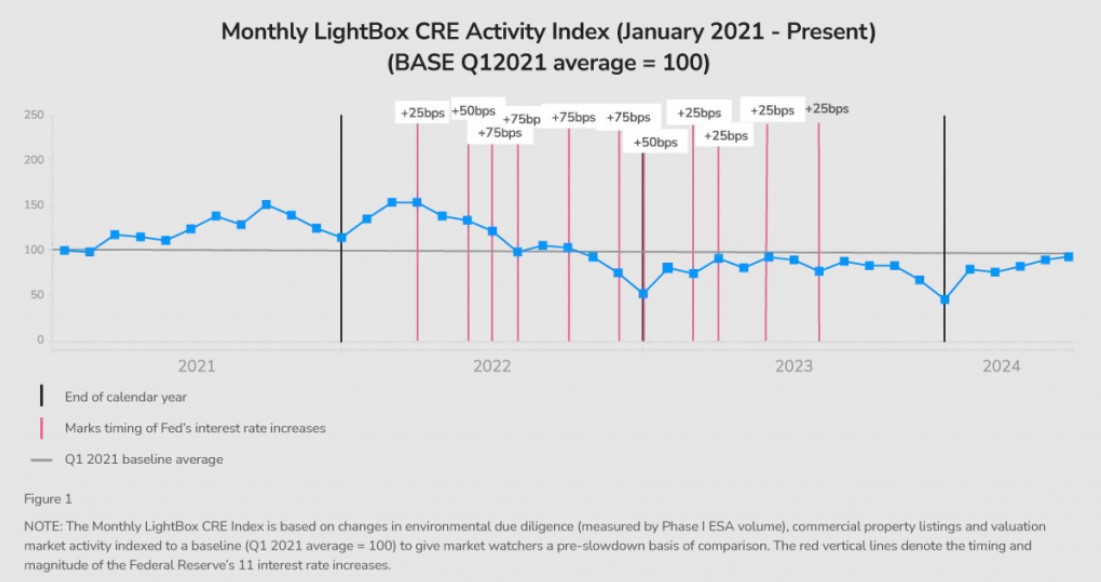

2. CRE POISED FOR CUTS

According to Lightbox’s monthly CRE Activity Index, CRE transaction activity has inched up every month since March, and the sector appears poised for a strong Q4, with the market anticipating one or more rate cuts by the end of 2024.

The index softened slightly in August, interrupting a five-month trend of modest increases. However, the analysts of the report did not consider the downtick a concern, with the August level still nine points above its level one year ago.

The year-over-year climb in activity reflects a CRE transaction landscape that is gradually thawing from a pricing standoff between buyers and sellers. As rate cuts filter into commercial mortgage borrowing rates, investors are likely to deploy more capital if current patterns hold, causing transaction activity to rise.

Still, investors will need to keep watch of a softening labor market and its potential implications on consumer spending and demand. It remains to be seen whether the Fed is ahead of or behind the curve on a rate pivot and can stave off an economic recession.

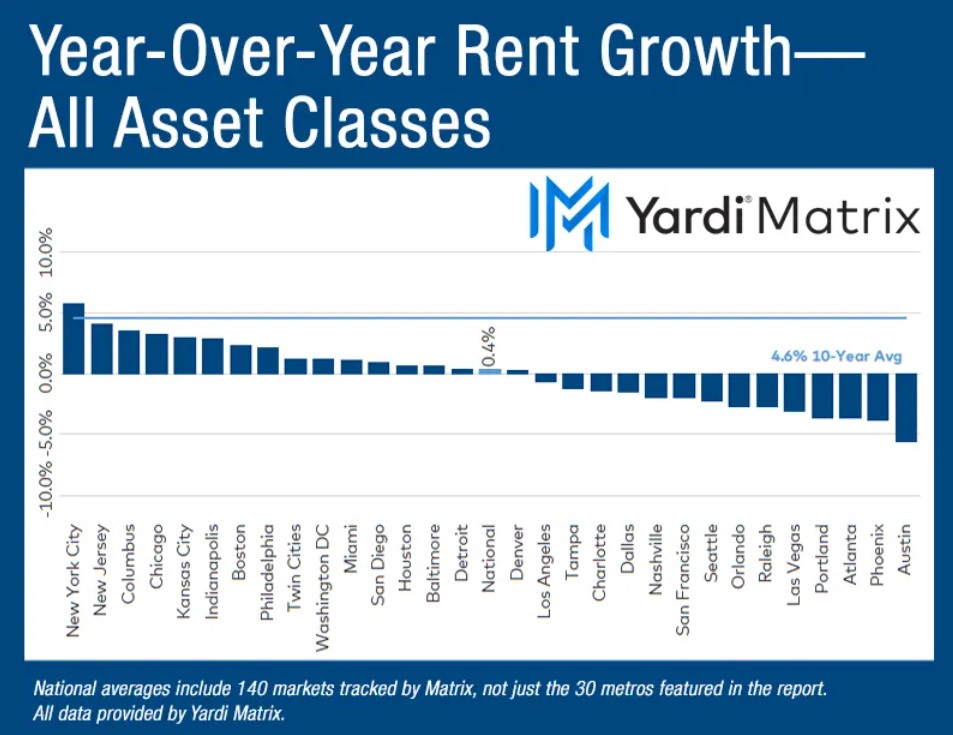

3. MULTIFAMILY AWAITS IMPACT OF SEPTEMBER RATE CUT

Multifamily rent growth was flat in August as shifting seasonality trends ended a six-month streak of growth, according to the latest Multifamily National Report by Yardi Matrix.

According to the report, the apartment sector is in a holding pattern as the market awaits an imminent September rate cut. Following the Fed’s anticipated move, a thawing of transaction and refinancing activity is expected to follow. An interest rate cut is also likely to reduce the pressure on underwater properties.

Still, as rates are poised to come down, the economy is showing signs of cooling, with slowing job growth and weaker wage growth compared to recent years. As the Multifamily market feels rate relief, a slowing labor market may place a drag on consumer and apartment demand.

4. ELECTION VOLATILITY

According to a recent analysis by Chandan Economics, market volatility typically spikes in the months leading up to a US presidential election, usually beginning to shift around July.

On average, during calendar years when there is a presidential contest, volatility, as measured by the CBOE Global Market’s Volatility Index (VIX), has tended to decline over the first seven months of the year before shifting higher during the final three months of the campaign.

In September and October of election years, the VIX has had an average value of 19.2 compared to an average of 18.2 during July.

The volatility experienced in stock markets over the past several weeks may, in part, reflect the typical election impact on markets and a market tendency that is in part independent of recent economic developments.

5. AUGUST JOBS REPORT

According to the BLS, the US economy added 142,000 jobs in August, above July’s downwardly revised increase of 89,000 but indicative of additional labor market cooling, with another downward revision in August likely.

The unemployment rate fell slightly to 4.2% last month, which put an end to a months-long increase in the unemployment rate that began in March.

Education, healthcare, leisure & hospitality, and government positions accounted for 117,000 of the 142,000 jobs added in August. However, new healthcare and government jobs have slowed notably. Professional & business services and information-related jobs remain subdued.

The number of people employed part time for economic reasons was little changed at 4.8 million, but the measure is still up from 4.2 million one year ago.

Average hourly earnings increased by 14 cents, or 0.4%, in August and are up 3.8% over the past year. Annual wage growth has gradually slowed from a post-2020 peak of 5.9% in March of 2022.

6. BEIGE BOOK

According to the Federal Reserve’s latest beige book of economic activity, nine (9) of the 12 Federal Reserve districts reported slow or declining activity, up from five (5) in the previous period.

Employment levels were steady across most districts, but there were notable reports of firms lowering overall employment through reducing hours, attrition, or only filing necessary positions.

Consumer spending fell after remaining steady throughout the previous period. Meanwhile, manufacturing activity declined in most districts.

On average, most districts reported mixed residential construction and softer home sales, while commercial construction and real estate activity were mixed.

7. RETAIL DURING THE POST-PANDEMIC PERIOD

As detailed in a recent analysis by Brookings on commercial real estate trends during the post-pandemic period, Retail was the most stable sector throughout the pandemic, balancing steady value growth with stable occupancy levels.

Despite a sharp rise in sector distress during the early days of the pandemic lockdown, retail demand has grown from its pre-pandemic levels, and rental properties have generated competitive returns.

Nationally, the Retail vacancy rate is at a five-year low and is the only product type for which aggregate vacancy has declined since 2019.

Still, these vacancy rates vary locally, and the variation often reflects increasing vacancies in downtown areas and retail inequality in minority-majority neighborhoods.

8. TRANSIT-ORIENTED DEVELOPMENT STUDY

A recent GlobeSt look into a study conducted by the University of North Texas Economic Research Group describes the impact of transit-oriented development on local economic activity in Dallas.

The study examined the impact of real estate developments near Dallas Area Rapid Transit (DART) light rail stations and found an increase in direction spending and job creation in those areas.

Focusing on 21 real estate developments built near DART stations between 2019 and 2021, the study found that collectively, the projects generated $980 million in direct spending and 10,747 jobs.

The projects encompassed a mix of commercial, residential, and public developments. They generated $144.7 million in federal tax revenue and another $49.6 in state and local tax receipts, according to the results of the analysis.

9. LOGISTICS MANAGERS INDEX

The US Logistics Managers Index ticked down slightly in August compared to July, but the report continued to point to a moderate pace of growth in the logistics sector.

Most notably, there was an increase in inventories as firms gear up for the holidays and Q4 spending season. August ended three consecutive months of contractions in inventory levels. The report also suggests that firms may be anticipating a return to the traditional patterns of seasonality not experienced since before the pandemic.

The effect of increased warehousing capacity and transportation capacity partly softened the rise in inventories.

According to the analysis, this is consistent with reports that firms are keeping most of their inventory near points of entry, waiting for them to move to retailers. Transportation prices eased compared to the previous month, while warehousing prices were up.

10. NFIB SMALL BUSINESS OPTIMISM INDEX

According to the National Association of Independent Business, small business optimism in the US declined in August to its lowest level in three months.

Inflation remains at the top of owners’ minds, and sales expectations have fallen significantly. Overall, rising uncertainty continues dominating movements in the index, with the outlook on future business conditions gradually worsening.

24% of small business owners cited inflation as their number one concern, while the net percent of owners expecting higher sales volumes fell to a net -18%. Meanwhile, 20% plan to raise compensation in the next three months, an uptick from the latest report.